Financial Planning

Why devote time and resources to financial planning?

- It forces us to think about what to do with money. It prevents money from working for other people's objectives and makes us manage it by orienting it towards our vital objectives.

- Avoid improvising. Less chance of making mistakes. Helps us to know ourselves and identify present and future needs, to maximize savings and to get into debt responsibly and efficiently.

- Avoid over-indebtedness. No need for personal loans and no need to use deferred payments with credit or revolving cards.

- It grows our wealth over the long term. Spending time planning grows personal wealth by an average of 20% per year*.

- It reduces the probability of conflicts in the family. It affects spending and saving decisions, coping in times of crisis, income level in retirement and the organization of succession.

- It transcends financial content. It affects the quality of family life, relationships, and even health.

- It is a powerful tool against the biases of impatience, immediate retribution, and lack of self-control.

WHAT IS PERSONAL FINANCIAL PLANNING?

What is Financial Planning?

Definition: is a standardized process designed to enable consumers to achieve their life-cycle objectives (section 3.14 of ISO 22.222). This process ensures a clear and effective structure for financial decision making.

- Standardized process means that it complies with a technical quality standard*, in this case ISO 22.222 for personal financial planning.

- Achieving life goals throughout the life cycle means scheduling and anticipating present and future life events, and being prepared for unforeseen events. This will allow you to reach retirement and beyond with the security of not having to change your standard of living or rely on third parties such as the state or your children.

Personal financial planning is done in steps, going into different areas of action; everything is explained in detail below in the section on how the service is provided.

* In accordance with Article 8 of Law 21/1992, a quality technical standard is a document of voluntary application containing technical specifications based on the results of experience and technological development. ... and must be approved by a recognized standardization body.

How is the service prepared?

According to the ISO 22.222 Technical Quality Standard, personal financial planning is developed in six key steps, which are reviewed and adapted throughout the relationship between the client and the planner.

This approach is not limited to a list of actions; it is a comprehensive process that connects all areas of a person's financial life. From budgeting, to debt management and investment, each step is designed to enable the client to organize his or her finances in a balanced and goal-oriented way.

STEP 1: ESTABLISH THE PROFESSIONAL RELATIONSHIP

Definition: is a standardized process designed to enable consumers to achieve their life-cycle objectives (section 3.14 of ISO 22.222). This process ensures a clear and effective structure for financial decision making.

- The scope of the service.

- The professional qualifications and experience of the professional who will provide the service.

- The method of work to demonstrate its conformity with the technical quality standard.

- The basis of remuneration.

- Any conflict of interest.

- Execution deadlines.

- The duration of the contract.

- Frequency of contacts.

- Confidentiality and data protection provisions.

Personal financial planning is done in steps, going into different areas of action; everything is explained in detail below in the section on how the service is provided.

* In accordance with Article 8 of Law 21/1992, a quality technical standard is a document of voluntary application containing technical specifications based on the results of experience and technological development. ... and must be approved by a recognized standardization body.

STEP 2: VITAL OBJECTIVES

During the financial planning process, the planner will conduct one or more personal meetings with the client in order to determine and understand the client's short-term and long-term life goals. These meetings are essential to establish direct and close communication, allowing the planner to obtain detailed information about the client's financial and personal goals.

- Vital objectivesare those activities or needs that the customer will satisfy in the current year (up to the end of the calendar year).

- Future life objectivesare those needs that the customer wants or has to meet in the future.

STEP 3: RESOURCES

The planner shall make and provide to the client, in a clear and reasonable manner, an evaluation of the client's status from a financial and economic point of view. This assessment shall be made using the balance sheet and the forecast income statement as tools.

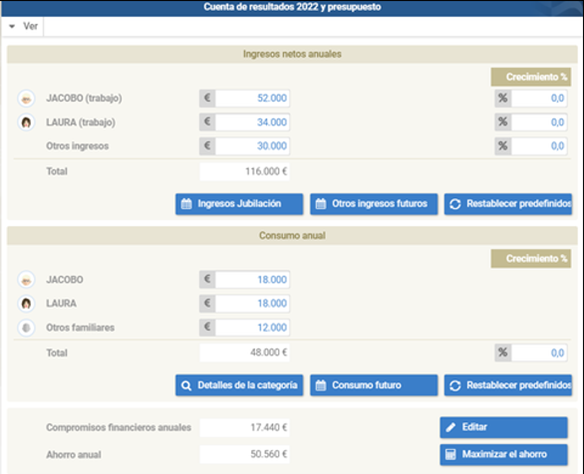

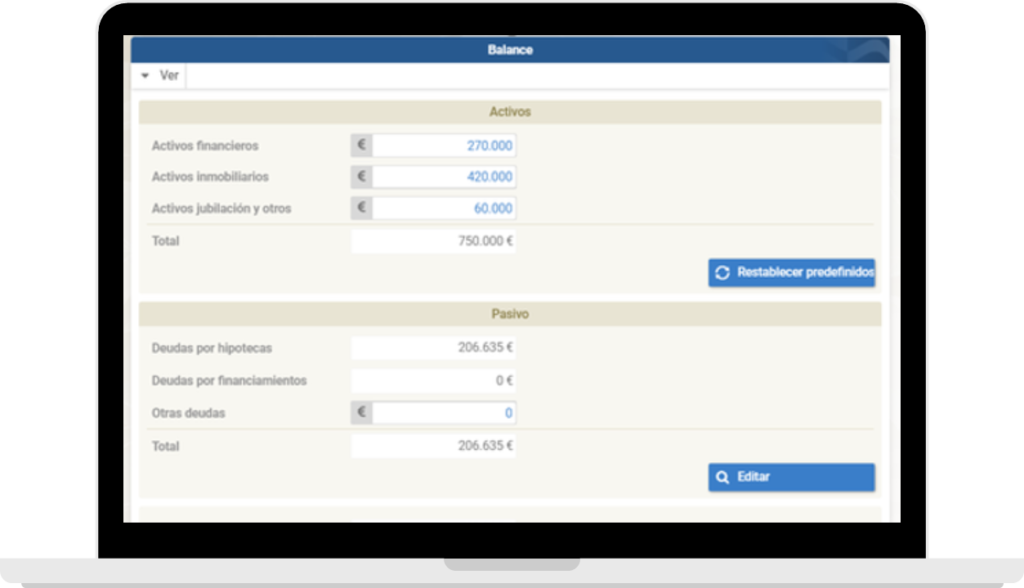

- BalanceThe client's financial situation: Collects and organizes all current assets and liabilities of the client and his or her family. With this information, you will get a complete picture of the client's current assets and you will be able to understand the client's true financial position.

- Pensionable income statementProjections of the family's future income and expenses. It allows to determine the desired level of savings to achieve the financial objectives set and to evaluate the feasibility of the proposed financial plans.

STEP 4: STRATEGIES AND PRESENTATION OF THE PLAN

It is time to define financial strategies for each key area: from organizing the budget and protecting assets and family with appropriate insurance, to planning for retirement or designing an investment plan.

All of these recommendations are compiled in a Personal Financial Plan Report, an essential document that provides a complete and personalized vision of the way forward. Prior to delivery, the report is thoroughly reviewed and validated with the client to ensure accuracy and clarity.

The planner accompanies the client at all times, resolving doubts and explaining each strategy, so that the client understands the plan and can implement it with confidence and commitment.

The Personal Financial Plan Report is a written document, personalized and tailored to the needs and goals of each client. It summarizes the strategies in each area of action and serves as a practical guide to effectively implement the plan with the financial intermediaries of the client's choice.

- Steps to follow:

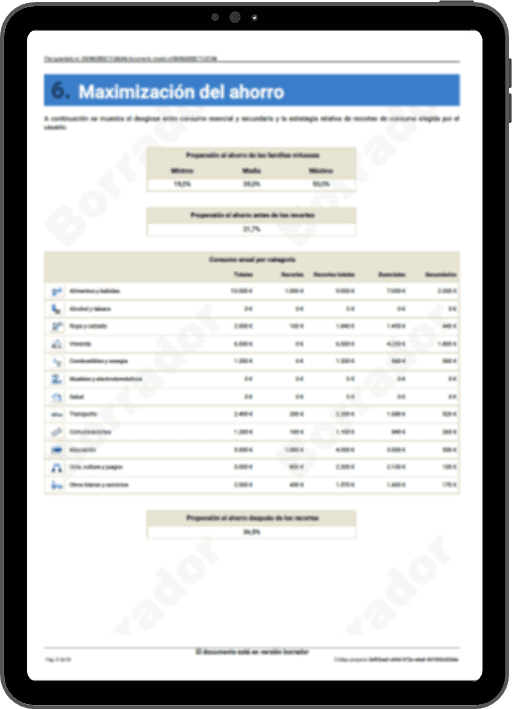

- Maximizing savings.

- Economic stabilization.

- Set the stability or emergency fund.

- Steps to follow:

- Set the retirement income target.

- Identify existing resources (public and private).

- Determine the need.

- Elaborate strategies with typology of complementary products (PP), investment and private funds (PIAS, retirement plans, rental income, other income).

- Steps to follow:

- Decide which assets and which family members should be covered, and which coverages (death and/or disability) for each person.

- Identify existing resources (public and private) for each contingency.

- Determine the need for private coverage.

- Develop strategies with own or external resources.

- Steps to follow:

- First, determine the liquidity fund and the reserve fund.

- Then, with the available financial assets and available savings, set the investment strategy that is efficient, effective and consistent with the client's life objectives and attitude to risk.

- Steps to follow:

- Set the indebtedness target.

- Set the indebtedness target.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

STEP 5: PLAN IMPLEMENTATION

Implementation is the stage where the plan becomes action. The planner accompanies the client to correctly apply the strategies, reviewing the current financial products and assessing new proposals from banks, insurance companies or other intermediaries.

Accounts, insurance, funds or investment plans are analyzed in detail, evaluating costs, conditions and benefits, in order to recommend whether to maintain, adjust or replace each product. At the same time, we review new alternatives that may better fit the client's objectives, always with an objective and transparent criterion.

During this process, the planner ensures that the client understands each decision and feels supported in negotiating with intermediaries. In addition, the implementation includes the incorporation of healthy financial habits: budget management, debt reduction and the creation of consistent savings.

The objective is clear: that the client can implement his plan with security, confidence and consistency.

STEP 6: FOLLOW-UP

Follow-up is key to keep the plan alive and useful over time. Life changes and so do finances, so the planner accompanies the client to adjust it whenever necessary. Follow-up includes:

Periodic reviews: recommended every quarter.

Extraordinary revisions: when a major change occurs in the client's life (family, work, health) or in the economic environment.

Group sessions and ongoing communication: shared learning spaces, sharing of practical information, regulatory developments and relevant opportunities to support client financial education.

In addition, the client can count on Plafira, an online tool that facilitates the updating and control of his plan at all times, guaranteeing accessibility and traceability; the objective is that it evolves with the client's life and continues to guide him towards his objectives.

WHY HIRE THE FINANCIAL PLANNING SERVICE?

First, we need to be aware that we need to have financial education and planning, tools and professional help.

Those who have less, who earn less, do not need more help, not at all, education and financial planning is like health, it is the person who has to take care of his health, it is the person who has to take care of his education and financial planning, therefore, we all have to have education and financial planning regardless of our level of income or level of wealth.

Second, look at ourselves and ask ourselves if we are managing our assets as well as we should.

We should ask ourselves whether we are using the right tools, whether the products sold to me by financial intermediaries are the best and most suitable, and whether I have the professional help I would like. If any of the answers are no or you have doubts, then you may be interested in contacting us.

EMPOWERED FINANCIAL EDUCATORS

The financial education and planning service offered by our company complies with the technical quality standard UNI 11402 «Financial education of citizens: service requirements», which defines the requirements for the design, implementation, delivery and evaluation of this activity and the requirements of the providers of this service.

The service is offered through AEPF-certified financial educators who have been trained and equipped with approved IT tools for the development of personal projects in accordance with the quality requirements of the technical standard.

Periodically AEPF, the financial educators and the tools used are reviewed by an independent external audit that guarantees maximum reliability, rigor and consistency with technical standards (Photo: audit certificate in force).

Security Guarantee

Going to a licensed professional guarantees a transparent and responsible service.

Quality Assurance

It guarantees that the professional who assists us has the necessary knowledge and skills to provide the service in compliance with the technical quality standards.

Guarantee of Professionalism

The qualification of professionals is audited and periodically updated by an authorized external institution (AEPF).

Warranty Claim

Possibility to turn to a third party institution (the AEPF) in case of disagreement with our services.

Results Guarantee

The citizen receives in writing a work carried out with tools that comply with the standard.

CONFIDENTIALITY AND PRIVACY

Need to Contact Us?

Book an appointment

Our professionals are registered in:

Business Program

Do you have a company or are you responsible for HR and want to improve the financial literacy of your staff?

Find out what benefits you can get with our corporate social welfare services.

Why address the welfare of workers?

In Spain, companies and social partners know how important it is to have conscious and serene workers, who do not live under the pressure of economic problems, who have the means to protect their families and can achieve their life goals.

Companies that are professionalizing corporate wellness programs and incorporating quality financial education programs get more satisfactory results.

The results measured show a strong improvement in the economic and psychological conditions of workers and families, with a particular benefit for separated workers, singles or singles with children, fragile categories that need awareness and work on their current and future bottom line.

The key is to have the figure of the “Welfare Manager”, a professional with the competencies and tools to carry out the corporate wellness plan following recognized quality standards.

In this sense, AEPF offers companies the possibility of improving or implementing a corporate wellness program based on quality technical standards, or simply improving the financial education of their employees through our YoWelfare program.

Children and Youth Program

CS Financial Planning, next to the AEPF, We promote the dissemination of financial education in schools through specific projects, based on simple and empathetic communication. With programs and didactic tools to bring financial education to the classroom and also aiming to involve parents in the process.

Yo-Welfare Kids & Junior

Program Yo-Welfare Kids for children between 5 and 13 years old in the early childhood education stage:

Tools to help them make decisions about how to talk about money in the home.

Games to learn the importance of saving, responsible spending and solidarity.

Strategies to stimulate conversation skills in the classroom and at home.

Yo-Welfare Family Program

Parents are a key reference point in this process. They are offered financial education programs designed to improve family communication and help their children manage money better.

Teacher training

We offer training and didactic material for teachers to teach financial education programs adapted to the technical quality standard. UNI 11402 financial education.

Children and Youth Program

CS Financial Planning, next to the AEPF, We promote the dissemination of financial education in schools through specific projects, based on simple and empathetic communication. With programs and didactic tools to bring financial education to the classroom and also aiming to involve parents in the process.

Yo-Welfare Kids & Junior

Program Yo-Welfare Kids for children between 5 and 13 years old in the early childhood education stage:

Tools to help them make decisions about how to talk about money in the home.

Games to learn the importance of saving, responsible spending and solidarity.

Strategies to stimulate conversation skills in the classroom and at home.

Yo-Welfare Family Program

Parents are a key reference point in this process. They are offered financial education programs designed to improve family communication and help their children manage money better.

Teacher training

We offer training and didactic material for teachers to teach financial education programs adapted to the technical quality standard. UNI 11402 financial education.

Business Program

Do you have a company or are you responsible for HR and want to improve the financial literacy of your staff?

Find out what benefits you can get with our corporate social welfare services.

Why address the welfare of workers?

In Spain, companies and social partners know how important it is to have conscious and serene workers, who do not live under the pressure of economic problems, who have the means to protect their families and can achieve their life goals.

Companies that are professionalizing corporate wellness programs and incorporating quality financial education programs get more satisfactory results.

The results measured show a strong improvement in the economic and psychological conditions of workers and families, with a particular benefit for separated workers, singles or singles with children, fragile categories that need awareness and work on their current and future bottom line.

The key is to have the figure of the “Welfare Manager”, a professional with the competencies and tools to carry out the corporate wellness plan following recognized quality standards.

In this sense, AEPF offers companies the possibility of improving or implementing a corporate wellness program based on quality technical standards, or simply improving the financial education of their employees through our YoWelfare program.